By Kathryn M. Kaminski and Yingshan Zhao at AlphaSimplex Group: In recent years, there has been a new trend towards creating ETFs that use Managed Futures strategies. Unlike other vehicle types, ETFs are often “beta”-oriented. There are different options for creating beta-like products for Managed Futures ETFs. Given this growing trend, this article reviews three different approaches for ETF design.

We start with two often-used methods: Index Replication and Mechanical Replication. Index Replication seeks to be consistent with the overall Managed Futures industry by tracking common yet un-investable indices.[1] Mechanical Replication is a direct implementation of a strategy using specifically selected models. For ETFs, this is generally a smaller and more basic set of models than the selection used in a mutual fund. For simplicity, in this article we’ll focus on trend-following models. Finally, we consider a hybrid approach, “Informed Index Replication,” that utilizes direct strategy implementation insights combined with Index Replication techniques, and discuss the strengths and weaknesses of different approaches for achieving beta exposure to Managed Futures.

Methods for Achieving Managed Futures Beta Exposure

Beta is a relatively clear concept in equity markets: what is the expected movement of a stock in comparison to the market as a whole (using an index like the S&P 500). However, this concept is less clear in the Managed Futures space, so it is important to highlight a few of the challenges in defining beta exposure in the space. First, the commonly-used indices are composed of manager returns from a variety of vehicles, including those that are not available in a ’40 Act vehicle with daily liquidity. This means that to replicate the index would require gaining access to an uninvestable basket of managers, or, more practically, that a beta strategy would need to track what the managers are doing from returns and industry insight. In addition, these indices generally change over time as the manager universe changes and as the managers themselves make changes to their process. Given this complexity, there are two common methods that can be used to capture a similar return profile: Index Replication and Mechanical Replication.

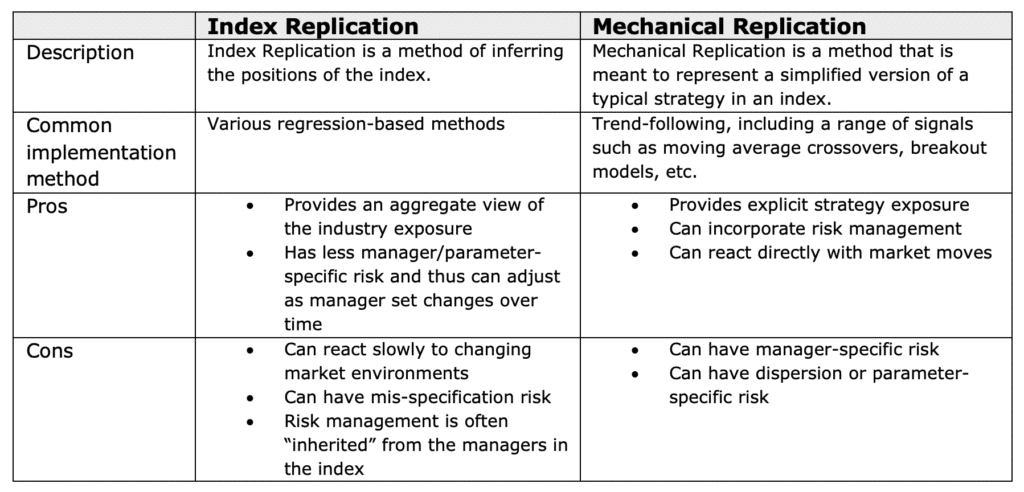

Index Replication is a method that infers the positions of index constituents in order to track the index. Common methods used to infer positioning include regression-based estimation on past index returns. Mechanical Replication, on the other hand, is direct implementation of a strategy similar to those utilized in the index itself, generally using a simplified version of the basket of strategies applied in the index. These approaches are often applied on a smaller set of markets and rely on the specific manager’s choice of parameters and strategies. The most common strategy in the space is trend following; common signals for implementing this strategy include classic signals such as moving average crossovers, breakout models, and other techniques. Both Index Replication and Mechanical Replication can achieve reasonable correlation to the commonly-used manager-based return indices, but there are pros and cons to each of these approaches (see Table 1 below).

Pros and cons of replication techniques for Managed Futures

Evaluating Different Replication Methods

As seen in Table 1, Index Replication has the benefit of tracking the industry profile to provide a return profile consistent with a basket of managers. The challenge with this approach is that it may react slowly to changing market environments because it uses past information to infer positions. On the other hand, Mechanical Replication provides a simplified model approach to capture the industry profile, but may suffer at times because it is only one strategy compared with a basket of strategies. Given these pros and cons, we also consider a hybrid approach to capturing beta exposure: Informed Index Replication, which combines Index Replication with insights from direct strategy implementation and adds risk management. To evaluate how well these techniques create beta, we consider three approaches: 1) Index Replication, 2) Mechanical Replication, and 3) Informed Index Replication.

As a proxy for each method, we consider a returns-based regression applied to the BTOP50 Index for Index Replication and a representative trend-following strategy based on direct signals for Mechanical Replication. For the Informed Replication, we use a Bayesian regression method that can incorporate information from direct strategy implementation. For our analysis, since the goal is replicating Managed Futures beta exposure, we consider three key metrics: 1) correlation, 2) tracking error, and 3) goodness of fit (or R^2) to the BTOP50 Index as measures for comparison. To maintain consistency across comparisons, the number of assets utilized in each method is the same: we include 20 contracts total, with five assets in each sector (equity futures, fixed income futures, currency futures, and commodity futures). We also scale the portfolios to a beta of 1 with the index to create a fair comparison using a rolling estimation window.

Correlation Over Time

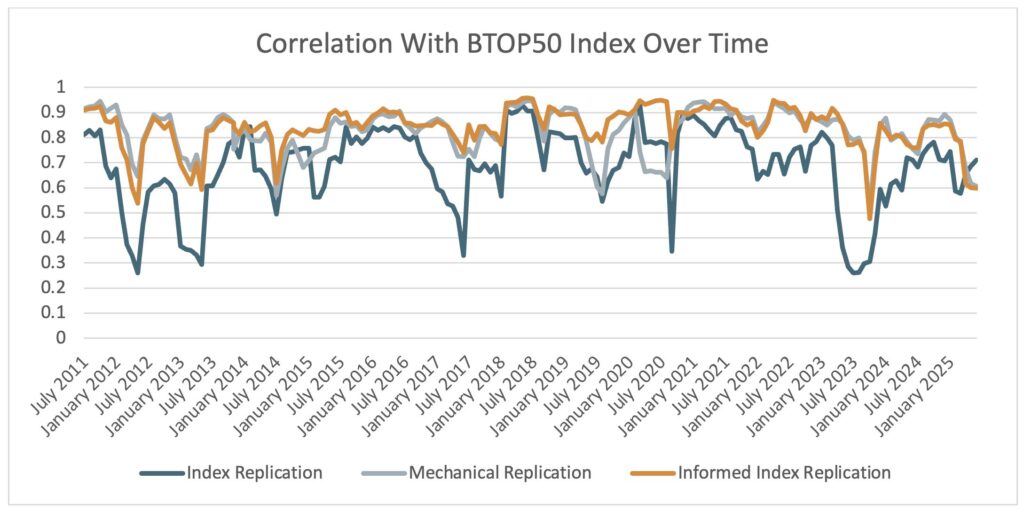

Although most Managed Futures funds often have high correlation to a representative index, correlation varies over time. Using each of the three methods described above, Figure 1 plots the correlation of each approach with the BTOP50 Index from Q3 2011 to Q2 2025.[2] From this figure, we can see that all three methods typically have relatively high correlations to the index. However, both Index Replication and Mechanical Replication seem to have certain periods where they exhibit lower correlation, especially Index Replication. In contrast, the Informed Index Replication approach that combines both techniques seems to achieve higher correlation across periods where either of the two methods diverges more from the index.

For example, the Index Replication method had a breakdown in correlation in 2020, during 2022, and during the second half of 2023. Each of these periods were periods where there were strong shifts in trends due to COVID-19, the Ukraine war crisis, and the end of the U.S. hiking cycle, respectively. This demonstrates that Index Replication can be slower to reflect large market shifts since it relies on past returns to indicate industry positioning. On the other hand, Mechanical Replication seemed to diverge during certain less descript periods, such as 2014 or 2019. This highlights the potential for parameter selection bias, where one strategy may have different positions than an index of combined manager returns. Finally, the Informed Index Replication technique seems to benefit from both approaches to achieve the highest index correlation over time. The intuition is that during periods of transition such as the Ukraine crisis in 2022 or the reversal period in 2023, combining direct signals with Index Replication can be more reactive than Index Replication itself. At the same time, following the overall CTA footprint can help a strategy be more aligned with the index than any individual strategy’s implementation.

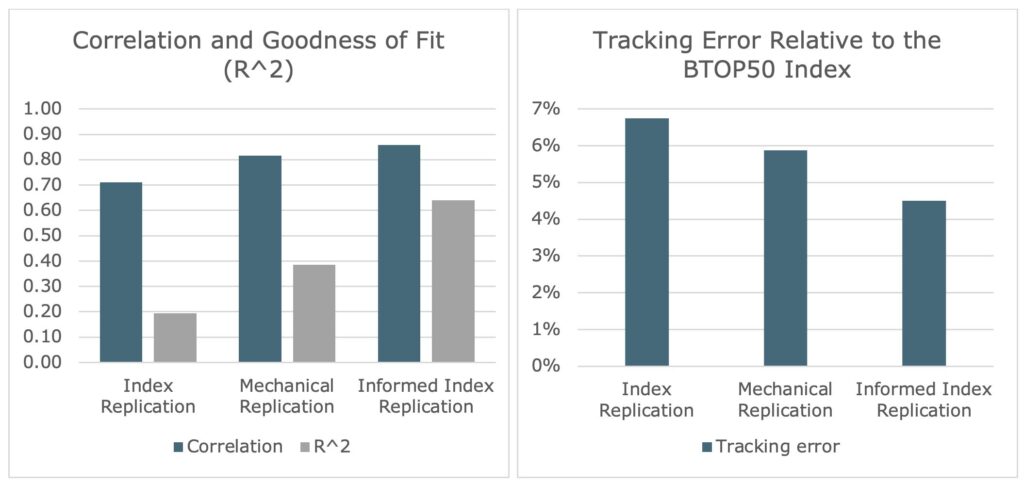

Next, we consider longer-term aggregate metrics for correlation, tracking error, and goodness of fit in Figure 2. From this Figure, we can see that Informed Replication has the lowest tracking error, highest correlation to the index, and highest goodness of fit to index returns of the three approaches. Mechanical Replication methods provide roughly 82% correlation and 5.81% tracking error but, as we see in Figure 1, there are occasional deviations that may impact the relative correlation over shorter periods of time. Putting this together, the results suggest that combining both methods may provide a more efficient method to achieve Managed Futures beta exposure with a goal of tracking the index and reducing some of the risks associated with an individual strategy like Mechanical Replication.

Summary

As Managed Futures ETFs gain in popularity, there are different methods for achieving beta exposure to the CTA space. In this paper we considered both Index Replication and Mechanical Replication, as well as a combined method we call Informed Index Replication. Using a simple proxy for each method with the same set of markets, we highlighted how Informed Index Replication had more persistent and higher correlation over time to the BTOP50 Index. Viewing correlations over time demonstrates some of the pros and cons of each approach. Informed Index Replication uses features of both methods and appears to benefit from the combination of replication styles over time. We also note that informed Index Replication provides the highest correlation and lowest tracking error to the BTOP50 Index, which suggests that combining insights of strategy implementation and index replication techniques can provide a method for achieving beta exposure to the index for ETF design.

[1] Common Managed Futures indices include the SG CTA Index, the SG Trend Index, the Barclay CTA Index, and the Barclay BTOP50 Index. We use the Barclay BTOP50 for comparison in this paper. This index is publicly available and includes the largest investable trading advisor programs. For more details, please visit barclayhedge.com.

[2] The period for analysis excludes the earliest history of the index. Over time the strategy set has changed for some managers included in the index. Therefore, the representative trend system chosen in this analysis is relevant for recent periods, but may not be as relevant for a longer study of the index since inception in 2000.

About the Authors

Kathryn M. Kaminski, Ph.D., CAIA® is the Chief Research Strategist at AlphaSimplex Group. As Chief Research Strategist, Dr. Kaminski conducts applied research, leads strategic research initiatives, focuses on portfolio construction and risk management, and engages in product development. She also serves as a co-portfolio manager for certain funds advised by AlphaSimplex. Dr. Kaminski’s research and industry commentary have been published in a wide range of industry publications as well as academic journals. She is the co-author of the book Trend Following with Managed Futures: The Search for Crisis Alpha (2014). Dr. Kaminski holds a B.S. in Electrical Engineering and Ph.D. in Operations Research from MIT.

Yingshan Zhao, CFA®, is a Research Scientist at AlphaSimplex Group. As a Research Scientist, Ms. Zhao focuses on applied research and supports the portfolio management teams. Ms. Zhao earned both a BSc. in Mathematics and Applied Mathematics and a B.A. in Economics from Peking University as well as an M.Fin from the MIT Sloan School of Management.

Disclosures

Past performance is not necessarily indicative of future results. Managed Futures strategies can be considered alternative investment strategies. Alternative investments involve unique risks that may be different from those associated with traditional investments, including illiquidity and the potential for amplified losses or gains. Investors should fully understand the risks associated with any investment prior to investing. Commodity-related investments, including derivatives, may be affected by a number of factors including commodity prices, world events, import controls, and economic conditions and therefore may involve substantial risk of loss.

The illustrations and examples presented in this document were created by AlphaSimplex based on unaudited data and methodologies. Accordingly, while the underlying data were obtained from sources believed to be reliable, AlphaSimplex provides no assurances as to the accuracy or completeness of these illustrations and examples. The views and opinions expressed are as of 6/30/2025 and may change based on market and other conditions. There can be no assurance that developments will transpire as forecasted, and actual results may vary. All investments are subject to risk, including risk of loss.

This document has been prepared for informational purposes only and should not be construed as investment advice. AlphaSimplex is not registered or authorized in all jurisdictions and the strategy described may not be available to all investors in a jurisdiction. Any provision of investment services by AlphaSimplex would only be possible if it was in compliance with all applicable laws and regulations, including, but not limited to, obtaining any required registrations. This material should not be considered a solicitation to buy or an offer to sell any product or service to any person in any jurisdiction where such activity would be unlawful.

Publication: September 2025. Copyright © 2025 by AlphaSimplex Group, LLC. All Rights Reserved.