Nordic high-yield bonds and the managers specializing in them have delivered strong returns in recent years, even outperforming local equity markets. Jarle Sjo, Head of Research at Norcap AS – Norway’s oldest independent investment advisor – notes that Nordic high-yield bonds have outperformed the Oslo Stock Exchange over the past three years. However, he cautions, “Past performance is no guarantee of future returns.” Despite this warning, Sjo points out that with yields in the Nordic high-yield bond market hovering around 7-8 percent, it would take a significant downturn for defaults and widening credit spreads to offset the interest income.

A Strong Year for High-Yield Bonds

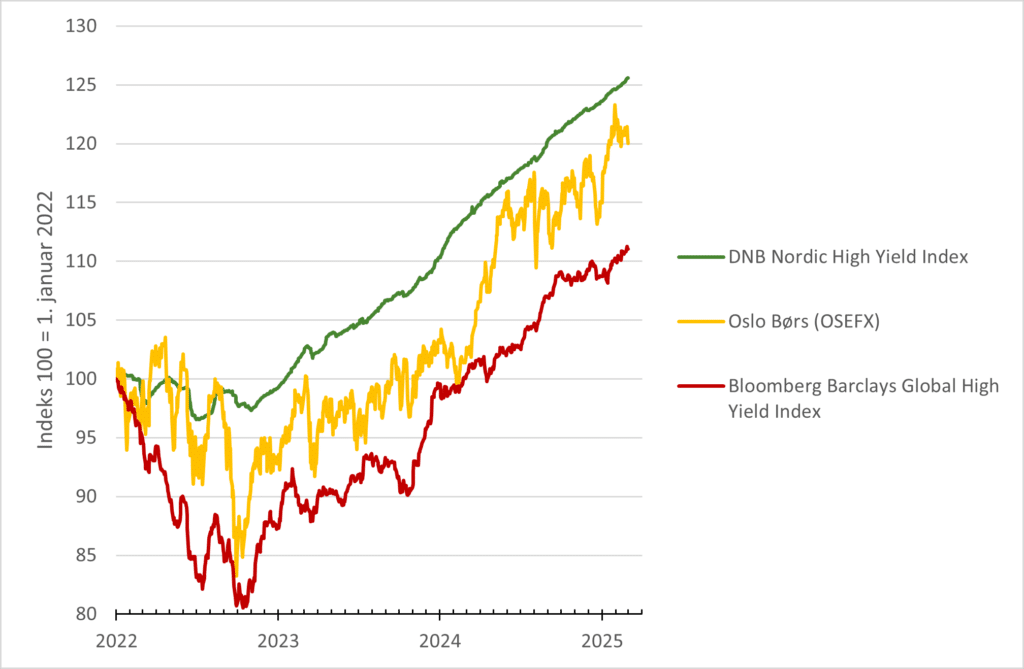

“Nordic high-yield bonds provided investors with high returns in 2024,” says Sjo, reflecting on the market’s performance. DNB’s high-yield benchmark, the DNB Nordic High Yield Index, rose by over 12 percent last year, “which is an unusually high return for bonds,” he notes. This performance came despite geopolitical turbulence and economic uncertainty. Looking at a broader horizon, Sjo highlights that over the past three years, “Nordic high-yield bonds have provided investors with better returns than stocks on the Oslo Stock Exchange.”

“Nordic high-yield bonds have provided investors with better returns than stocks on the Oslo Stock Exchange.”

Jarle Sjo, Head of Research at Norcap AS.

Since January 1, 2022, Nordic high-yield bonds have delivered returns of over 25 percent, outpacing the Oslo Stock Exchange, which has gained 20 percent over the same period. “Global high-yield bonds, by comparison, have returned only 10-12 percent, largely due to a weak development in 2022 driven by a sharp rise in interest rates,” Sjo points out. He explains that a key difference lies in interest rate structures: “Floating rates are more common in the Nordic high-yield market, whereas global high-yield bonds typically have fixed interest rates, making them more vulnerable to rising interest rates.”

Significant Dispersion in Fund Performance

While the broader Nordic high-yield market delivered strong returns in 2024, Sjo notes a wide divergence in both performance and risk among the individual high-yield bond funds his team tracks. “There were large return differences among Nordic bond funds specializing in high yield,” he emphasizes. The gap between the best-performing fund, Kraft Nordic Bonds, and the weakest, Handelsbanken Høyrente, reached as much as 24 percentage points.

“Although all these funds fall under the Nordic high-yield category, their risk profiles can differ significantly, making it challenging for investors to compare them.”

Jarle Sjo, Head of Research at Norcap AS.

“Although all these funds fall under the Nordic high-yield category, their risk profiles can differ significantly, making it challenging for investors to compare them,” concludes Sjo. “Some funds are more diversified, while others take on higher risk by investing in bonds with weaker credit ratings.”

Market Dynamics

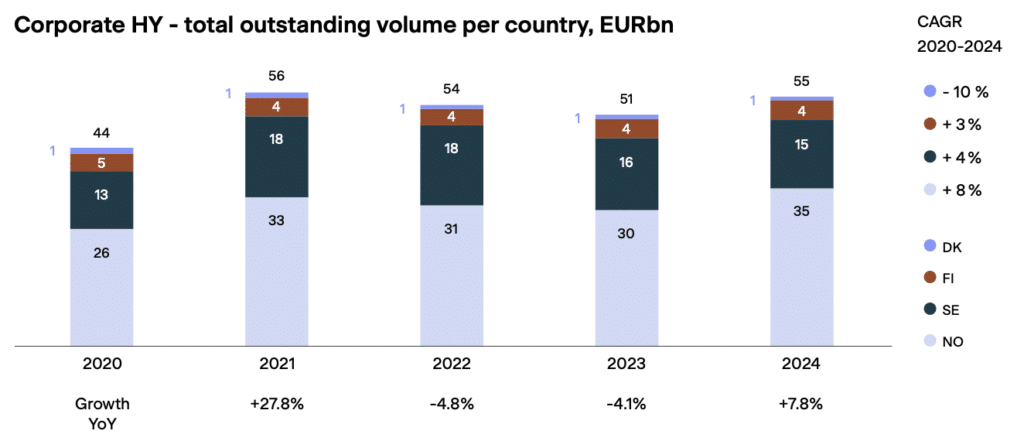

Beyond performance figures for bonds and fund managers, Norcap’s Head of Research has also noted significant growth in the Nordic high-yield market in terms of issuance, driven solely by growth in the Norwegian market, which was up 15.9 percent. By year-end, Norway accounted for 63 percent of all outstanding high-yield issuance volume, with Sweden following at 27 percent, according to the Nordic Trustee 2024 Corporate Bond Market.

“One reason for this increase in volume is the strong demand for high-yield bonds,” says Jarle Sjo. According to the Norwegian Securities Funds Association, net subscriptions to high-yield funds totaled NOK 32 billion in 2024, up from NOK 19.4 billion the previous year. Retail investors have also increased their allocation to high-yield funds, with their share of fund savings rising from 5 percent to 11 percent.

The high-yield market has become increasingly diversified in recent years. While real estate remains the largest sector, Sjo’s research indicates that the volume of issuances in other industries has grown significantly. The Nordic high-yield bond market has transformed into a more diverse universe, with issuers now spanning a broader range of industries. Once predominantly driven by real estate issuers, the market has expanded notably into sectors such as energy, shipping, industrials, and consumer goods. This diversification has helped mitigate sector-specific risks and provided investors with a wider range of opportunities. “The high-yield market has become more diversified in recent years and although real estate remains the largest sector, the volume has increased in other industries,” points out Sjo. However, regional disparities across the Nordic countries still persist.

“The high-yield market has become more diversified in recent years and although real estate remains the largest sector, the volume has increased in other industries.”

Jarle Sjo, Head of Research at Norcap AS.

The Norwegian high-yield bond market, for example, has seen significant growth in recent years and has become less reliant on the oil and gas sector. In contrast, the Swedish high-yield bond market has traditionally been concentrated in the real estate sector, with property developers and commercial real estate companies dominating issuance for years. This made Sweden’s high-yield market one of the most real estate-heavy in Europe. However, in recent years, the market has undergone a shift toward greater diversification, with increasing issuance from sectors such as industrials, energy, and consumer goods. Despite this shift, real estate continues to serve as the backbone of Sweden’s high-yield market.

Still High Yields, But Less Compensation for Risk

The default rate in the Nordic high-yield market rose throughout 2024, finishing the year at just over 5 percent. The real estate sector saw a default rate of 4.4 percent, while the energy sector ended at 3.6 percent. Notably, the real estate sector had reached a peak default rate of 8 percent earlier in the year before declining towards year-end.

When examining current yields in the Nordic high-yield bond market, Sjo observes that “interest rates are still high, but you get paid less for taking risk.” The yield to maturity for Nordic high-yield bonds is currently in the range of 7-8 percent. “Given that high-yield bonds carry a higher risk due to their weaker credit quality compared to investment-grade bonds, the probability of default is naturally higher,” he explains.

“While the interest rate on Nordic high-yield bonds has increased, much of this rise is due to higher market interest rates. However, the credit spread has been narrowing recently,” says Sjo. As shown in the figure from Alfred Berg below, the credit spread for Nordic high-yield bonds is currently around 4 percent, meaning investors receive an additional 4 percent return for taking on the risk of these bonds compared to a risk-free rate. “This represents the lowest credit spread in many years,” notes the Head of Research at Norcap AS.

“Although the returns in recent years have been good for Nordic high-yield bonds, it is important to recognize the inherent risks of these instruments,” warns Sjo. He recalls that in 2020, several high-yield bonds saw a sharp 25 percent decline in a short period. “When the pandemic hit, financial markets became volatile, investors pulled capital from riskier assets, and credit spreads widened. Additionally, significant currency fluctuations increased the capital requirements for hedging contracts, forcing funds to sell bonds to free up liquidity,” he recalls. “Liquidity in the market dried up, causing bond values to drop dramatically.” However, aggressive liquidity measures and interest rate cuts led to a market normalization within a few months.

In conclusion, Nordic high-yield bonds have delivered strong returns over the past three years, outperforming the Oslo Stock Exchange during the same period, according to Sjo. “However, past performance does not guarantee future returns. Despite current high interest rates, the credit spread remains low, which means investors are compensated less for taking on increased risk,” he emphasizes. Should market conditions become volatile, liquidity could decrease, and credit spreads could widen, leading to lower returns. “That said, with yields at 7-8 percent, the market would need to be particularly weak before defaults and higher credit risk premiums significantly offset the interest returns.”

“Ultimately, however, it is the managers who have a deep understanding of credit risk who are best positioned to deliver superior long-term performance.”

Jarle Sjo, Head of Research at Norcap AS.

“In the long term, high-yield bonds will provide good returns, but investors must brace themselves for fluctuations along the way,” concludes Sjo. “Some managers may achieve extra good returns in the short term by taking on higher risks in their portfolios,” he adds. “Ultimately, however, it is the managers who have a deep understanding of credit risk who are best positioned to deliver superior long-term performance.”