By Shaunak Amin and Joe Peta – Novus: Despite the hilariously outdated technology props and some extinct jargon, Oliver Stone’s Wall Street is still revered by financial industry insiders. Even today, more than 25 years after its release, Wall Street is regarded as a realistic depiction of the industry largely because the film nails the dynamics of some important relationships in the business.

Take the above quote, for example. Fund managers are perpetually being pitched. Sell-side analysts fill portfolio manager’s voice mails and inboxes with research ideas. Bankers want to bring their traveling roadshow to the buy-side office to pitch the latest company issuing paper. Today’s fund managers, just as Gordon Gekko implied, know how irritating it can be to face a bombardment of pitches that all look alike.

And yet, based on our discussions with allocators (endowment, pension, fund of funds or the like), when the tables are turned – when the hunted becomes the hunter – and managers need to do their own fund raising, many of them forget that very lesson.

Allocators who interview hundreds of managers each year tell us that it’s paramount for managers to distinguish themselves. One sure way not to do that is for managers to tell potential investors that they “have an edge” without accompanying evidence.

From the perspective of a hedge fund looking to raise capital, it can be perplexing to think about how allocators are making decisions about investing capital. One wonders if there is a clear path to moving things forward, and could one have improved the chances of getting a follow-up meeting? Let’s find out by getting into the minds of allocators.

SILLY BUT TRUE

- Allocators will prioritize a fund that is “soft-closing” vs. a fund that is perpetually open. It helps to have phases when you exclusively meet with allocators and other phases when you are focused on investing. It builds up demand. Deadlines help.

- Playing hard-to-get works.

- The biggest influence on investors’ opinions of a hedge fund is the opinion of other investors. There are very few who simply decide for themselves.

When an allocator hears about your hedge fund from a peer at another firm, you’ve already done the heavy lifting. To this point, it can help to have a mind map of who knows who. Similarly, the same effect can cause one allocator to redeem when someone else is redeeming.

- The story is what people remember.

- Like it or not, your fund is “bucketed” in a particular strategy/style in the allocators’ book. Knowing your “bucket” helps anticipate questions.

HOW CAN A HEDGE FUND HAVE AN EFFECTIVE FIRST MEETING THAT RESULTS IN A FOLLOW UP?

In a typical year, an allocator meets with hundreds of hedge funds. Most first meetings tend to be centered around topics like pedigree, research process and edge, ideas and theses on those ideas. After an allocator has 20 of these meetings, the story starts to sound the same. This routine does not give an allocator a true sense of what makes a manager unique. An open-ended meeting is often ineffective and results in no clear next step.

A better way to differentiate your value proposition

One of the most common questions an allocator is trying to answer is “What’s the edge?” While the question itself oversimplifies investing and carries some implicit assumptions, a simplistic, unsupported answer like “Our edge is security selection/research” by itself does not hold much weight. Talking about one or two high-conviction names does not really answer the question either.

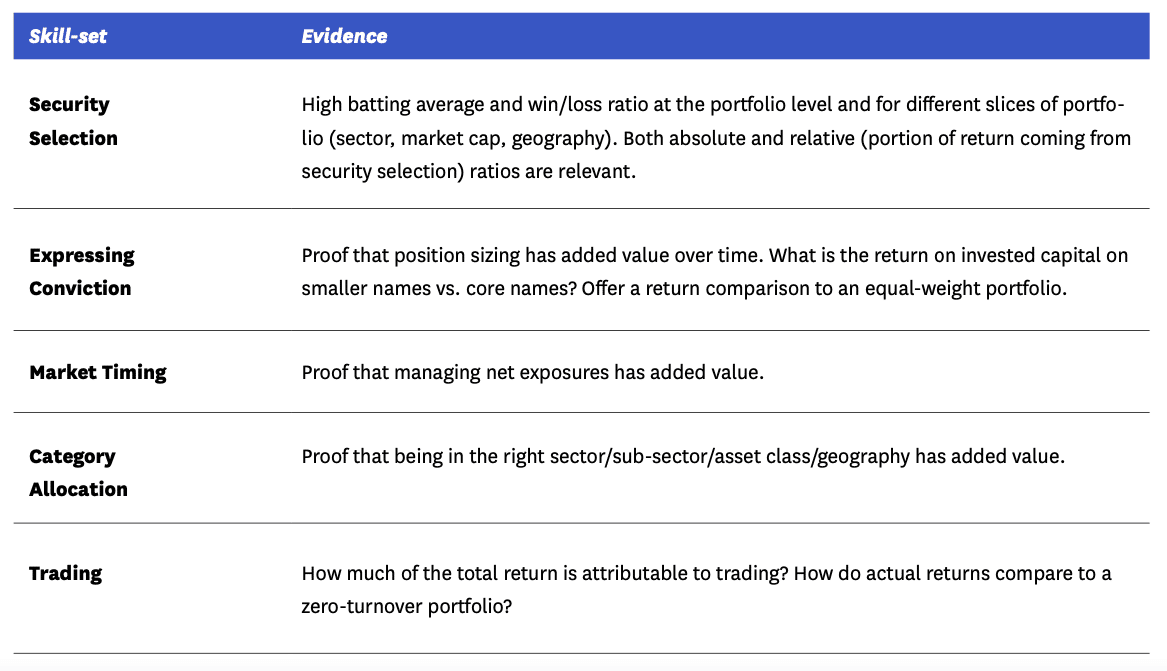

For the first meeting to be effective, a hedge fund manager must clearly articulate the value proposition to prospective allocators. Numbers and actual unadulterated statistics are more impactful than esoteric conversations around processes. For example, if research and security selection are indeed core drivers of returns, a more thoughtful answer would involve statistics that prove a manager is actually a good stock picker. One approach to highlight persistent security-selection skills would be to lay out batting average and win/loss ratios by sector/market cap/position size/liquidity or any other category that is most relevant. The table on the previous page lists a variety of skill-sets and how to present evidence of their existence.

Consider that for the first meeting to be effective, it is important to share with allocators:

- The true value proposition, supported by skill-set-centric results.

- The elements that differentiate your fund from other hedge funds.

What not to focus on in the first meeting?

The risk in covering too much in the first meeting/ call is that allocators spend 90% of the time on a topic that makes up less than 10% of the book and is not core to the overall strategy. These topics could be P&L derived from IPO’s or a few private positions that make up a tiny portion of the book. This is often unintended and it should be avoided.

The goal of the first meeting is to take baby steps to get to the second meeting; spending too much time on a small portion of your book can derail the conversation.

WHAT IS EFFECTIVE HEDGE FUND MARKETING?

The world of marketing has changed, and it’s critical for managers to rethink how they communicate with investors by taking a moment to see things from the investor’s point of view.

Investors today have access to more information than they can effectively consume. They are being bombarded by emails, marketing brochures, pitch books, and bold claims from managers competing for their capital. Increasingly, this sort of “push marketing” is having less impact on investors who have heard it all before. To be competitive in today’s environment managers need to differentiate themselves by clearly demonstrating their value to the investor through data-supported narrative.

An increasing number of innovative managers have evolved their marketing efforts by tapping technology and data analytics to help them quantify the value they deliver. Through the use of portfolio intelligence tools, they have gained an edge in raising and retaining capital.

Demonstrating their skill and highlighting the drivers behind their investment process, these managers can substantiate their claims and win the trust of investors along with their capital. In the meantime, managers who continue to rely on subjective claims alone will be at a significant disadvantage, even if they are as skilled as they claim.

Here are four specific steps to take your marketing to the next level:

- Focus on what makes you unique

Investors are looking for unique opportunitiesnot another “fundamental l/s” fund. Focus on your key differentiators and connect them to your background and expertise.

- Align your message with the objectives of your investors

Investors from pensions to funds of funds are faced with criticism of putting up with sub-par returns, paying high fees and not fully grasping the complexities and risks of hedge funds.

Whether they are looking for uncorrelated sources of returns, absolute returns, or alpha, it is your job to understand investor needs and challenges.

- Talk about your “fund” as a business

Besides running a portfolio, you are running a business, and investors are keen to understand the strengths and challenges of your organization.

Organizational structure is often highlighted in marketing documents but few talk about organizational ‘health’. What is the reason the fund was launched? What are your beliefs and guiding principles? If you are clear on those and you dedicate time to them in your messaging, you are more likely to attract strong, long-term partners who share your values.

The rest of the article will focus on our final point – and one we feel is most critical in separating effective marketing from mediocre. It is the ability to show value rather than just tell folks about it.

- Show, don’t tell

A picture is worth a thousand words. In our day and age, it’s worth a lot more since no one has the time to read a thousand words but they are happy to quickly glance at a chart and discover the insight for themselves. Of course, it’s critical which data you choose to visualize.

This article features in HedgeNordic’s “Powering Hedge Funds” publication.