(Partner Content – CME Group) – With the ongoing impact of COVID-19 combined with geopolitical tensions affecting volatility, Phil Hermon and Craig LeVeille of CME Group explain how new analytics are affording traders more visibility than ever before into the FX marketplace to help identify potential investment opportunities.

It is fair to say that markets have seen periods of great uncertainty during 2020. A myriad of events from the COVID-19 pandemic, to large political milestones such as the US election and the Brexit talks, continue to create a challenging environment for traders. This unique set of circumstances may set the conditions for traders to explore new ways of doing business in order to help them better identify potential opportunities and to optimize how they access the market.

Back in March, the OTC FX swap market struggled globally as a result of the COVID-19 induced volatility. Initially there was a flood of interest in the US dollar, as investors sought a safe haven during an unprecedented period of stress. Then, during Q3, investors decided to position themselves against the dollar and so moved back to currencies including the euro, Swiss franc and Japanese yen.

Following a 27 year low in volatility for FX in January of 5 percent, the FX options market also saw their fair share of uncertainty as the impacts of COVID-19 were felt across global markets ‒ resulting in a 10 year high of volatility in March of around 15 percent. In addition to the pandemic, the continued uncertainty surrounding the future trading relationship between the UK and the EU in September sent sterling to its lowest point since March, triggering a surge in volatility.

A more constant theme for clients, however, is continued investor pressure for improved performance, coupled with heavy regulatory disclosure burden from MiFID. Both these factors are catalysts for change and drivers behind traders looking for more transparency to help identify potential investment opportunities.

In response, we have launched two tools to help deliver unprecedented levels of transparency, helping FX traders to more easily monitor price relationships, make more informed decisions across markets, and ultimately, ensure best execution for their trading strategies.

The FX Options Volatility Converter “Vol Converter” tool

As markets become increasingly volatile, the search for high-quality liquidity intensifies. As a result, FX traders are understandably looking to compare prices between both OTC and listed FX options markets to ensure they are delivering best execution throughout this unpredictable period.

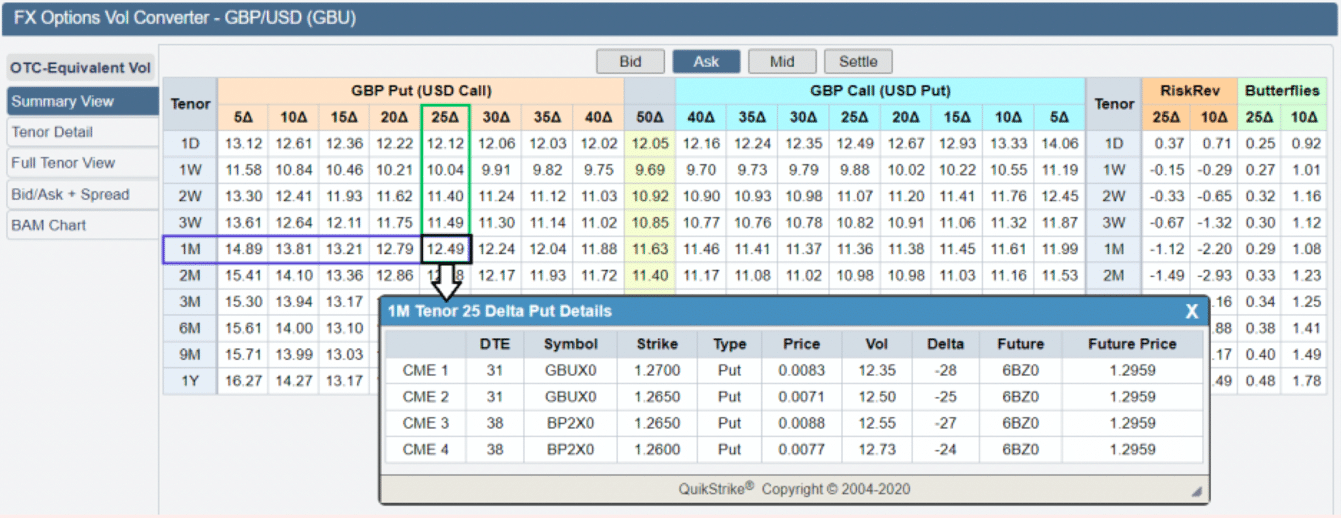

Best execution could very well be taking place in an OTC liquidity pool, but how can an FX trader be 100 percent sure it is the best possible price? Particularly, if they are unable to compare prices across multiple different liquidity pools. Only by adding listed venues into the mix, can the chances of achieving the best possible price between OTC and listed FX options increase. Our FX Options Vol Converter tool, released in September, summarizes thousands of data points into one single volatility surface for easy viewing. This allows FX traders to quickly pinpoint the most relevant instruments for their trading strategy.

Take the example of an FX trader receiving offer quotes for 7.85 percent and 7.90 percent from two OTC pricing sources for a two-week 35-delta EUR/USD options contract. The trader may want to compare these pricing sources with options pricing available on our venue. He or she could go into the tool to find that comparable instruments to the two-week 35-delta EUR/USD options contract are being offered at an implied volatility of 7.63 percent.

Take the example of an FX trader receiving offer quotes for 12.75 percent and 12.80 percent from two OTC pricing sources for a 1 month delta GBP/USD options contract. The trader may want to compare these pricing sources with options pricing available on our venue. The trader could go into the tool to find that comparable instruments for that tenor/delta combination are being offered at an implied volatility equivalent to 12.49 percent.

This could actually be a better price than what was quoted in the OTC market. By clicking on the displayed volatility, the trader can see a list of the FX options instruments that most closely contributed to the implied volatility data point. The trader has all the information needed to quickly assess the alternatives, select the contract on their CME trading system, and execute on the trade if desired.

It is easy to see how this tool boils down the complexities of comparing options on futures and OTC options into a few steps, allowing traders to be efficient and more aware of opportunities. More than 1,400 FX participants have viewed the tool since its launch, and over a quarter are repeat users clearly enjoying the access to live quotes from a highly competitive, transparent options market.

The FX Swap Rate Monitor (FXSRM) tool

Over half of the $6.6 trillion a day global FX marketplace is made up of FX swap transactions, the majority of which are traded bilaterally on a request for quote (“RFQ”) basis. Whilst spot FX, FWDs, and NDFs all have primary venues and central limit order books to assist with price discovery, the FX swap market remains largely bilateral between clients and their panel of bank liquidity providers.

Due to this market structure, buy-side traders will need to work with each of their liquidity providers to understand where the market is trading and what prices they can get on specific transactions. The FX Swap Rate Monitor is, however, now providing additional market color to augment this process for traders. The FXSRM displays current market prices for a credit agnostic and centrally cleared FX swap alternative, and as such, the bid, mid, and ask displayed can be used by traders as a reference point for where the market is trading.

Additionally, the FXSRM tool calculates and displays the implied interest rate differential by using the underlying data from CME FX futures along with the spot-futures basis in CME FX Link’s central limit order book, in order to derive a spot rate. As such, the tool is calculating implied interest rate differentials based on actual pricing data from a very large and diverse FX marketplace which can also be used by traders to help identify potential investment opportunities.

Interest rate differentials between currencies are a crucial input for any trader active in the forwards market, but the drivers and exact level of the interest rate differential are not always easy to see. Whilst economic theory suggests the differentials should be almost purely driven by the underlying short-term interest rates available in each jurisdiction, the data suggests that other meaningful forces of supply and demand are very much at play. Erik Norland, Senior Economist at CME Group, recently wrote a paper looking at these differences, providing worked illustrations as to how the implied interest rate differentials have diverged from OIS rates over the course of 2020.

This divergence in implied interest rates, apart from what economic theory suggest they should be, is a demonstrable example of how traders can benefit from a tool that provides a real and current market view of where the FX swap market is trading and what the associated implied interest rate differentials are. This tool should help in making sure their pricing of FX forwards is correct, and of seeing if there are alternative investment opportunities available to them.

Moving forward…

The backdrop of COVID-19, geopolitical uncertainty, and new regulations will continue to bring attention to the global markets in the weeks and months ahead. As the world reflects on the events of the year to date, people’s attention will soon turn to what is potentially to come.

One thing is for certain, the topsy turvy time experienced by FX swaps and options markets is unlikely to go away anytime soon. With this in mind, we feel our recent market innovations provide some much-needed light at the end of the tunnel. Market participants can now, for the first time in the history of the FX market, have full visibility into the bid and ask, and mid-market rates for swaps on a Central Limit Order Book (CLOB).

Similar to the benefits of our FX Options Vol Converter tool, these prices are available to all market participants ‒irrespective of credit rating. So, whatever the world has in store for markets down the road, at least by finally being able to compare and contrast their bank prices when asked about where the market is trading, traders will progress in addressing the longstanding issue of increasing transparency in FX.

View the FX Options Vol Converter →

View the FX Swap Rate Monitor →

Title Pic: (C) spectrumblue—shutterstock.com