EM ESG Fixed Income Strategies Pass Their First Stress Test

By Jens Nystedt and Oliver Faltin-Trager, Emso Asset Management – In recent years, ESG has commanded significant interest from investors across all asset classes, including emerging markets fixed income. As EM ESG fixed income mandates and benchmarks are still relatively young, the March 2020 market shock served as the first major stress test for such strategies. Overall, when compared to their non-ESG counterparts, we feel that the performance of these ESG mandates during the sell-off and the subsequent recovery will likely be an important driver for the pace of ESG asset growth and investor interest going forward.

Financial markets came under intense pressures in March as the world-wide lockdowns to combat the Covid-19 outbreak essentially shut down the global economy. EM fixed income assets were no exception to the pressures of Covid-19, and, as a result, they suffered significant losses as the overall shock was magnified by a poorly-timed oil price war between Russia and Saudi Arabia that weighed heavily on oil-exporting countries and their corporates. Market liquidity conditions were also quite challenging as market participants were forced to relocate to work from home setups or disaster recovery locations. This made it particularly challenging for EM to deal with large outflows, as many investors, particularly those that are retail based, headed towards the exit. In the months following, there was an unprecedented recovery across markets that was driven by the incredible fiscal and monetary stimulus actions from governments and major central banks. Looking back, the period from March to July gives a unique timeframe to analyze how ESG indices and mandates performed during a crisis and resulting market rebound.

These mandates have grown exponentially in a very short time. J.P. Morgan’s EM ESG benchmarks launched in April 2018, and within just two years, the benchmarks saw growth to over USD 13 billion of assets that are currently tracking them. After the Covid-19 sell-off, J.P. Morgan expects that overall assets that track against their benchmarks will grow to over USD 20 billion by year-end.

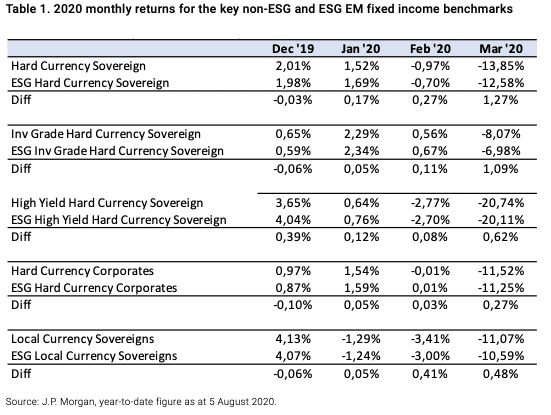

EM ESG fixed income indices outperformed the traditional EM fixed income benchmarks during this period, as shown in Table 1 below, and were accentuated by smaller drawdowns in March. While there was outperformance across the EM ESG sub-strategies, we found that the extent of outperformance was determined by the ESG benchmark’s overall reduced exposure to lower-rated issuers and oil producers. In the case of hard currency sovereigns, the ESG benchmark outperformed its non-ESG counterpart by nearly 1.3% during March alone. In our view, such outperformance for a year would typically be quite impressive and to achieve that in one month alone is quite exceptional. The degree of outperformance across all EM ESG fixed income categories during March provides a strong foundation to support the view that EM ESG benchmarks are capable of outperforming non-ESG benchmarks during market sell-offs.

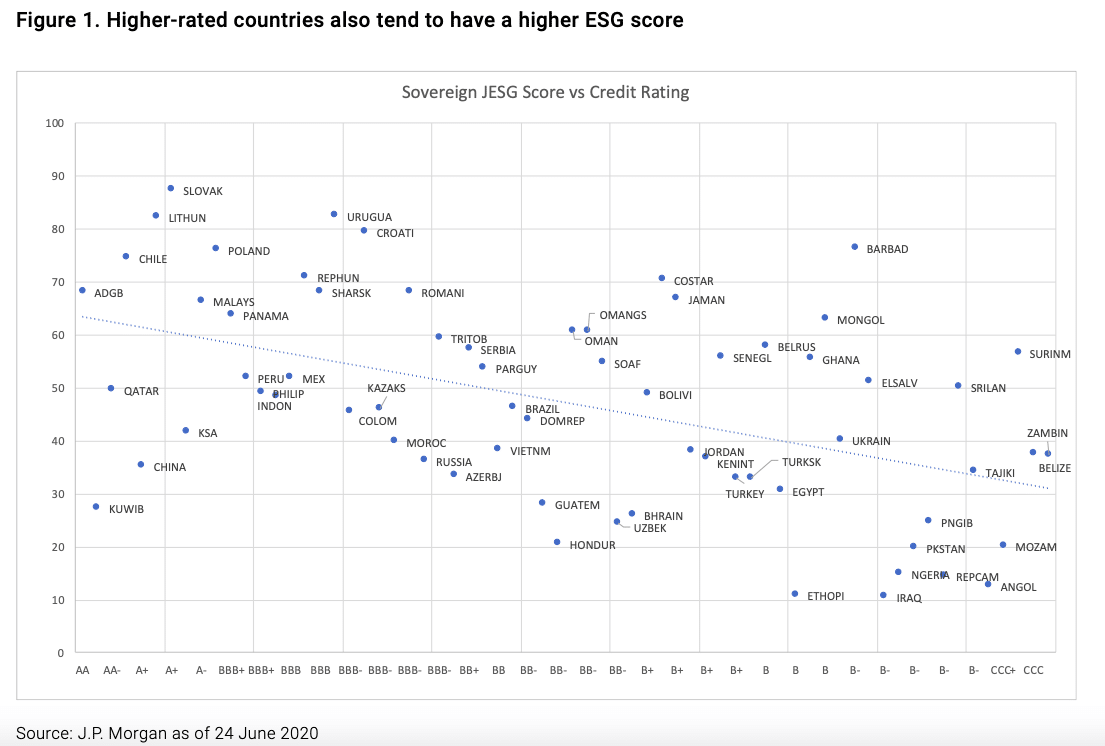

When analyzing the source of the outperformance, it is not surprising that EM investment grade issuers, whether sovereign or corporate, outperformed high yield issuers during the March sell-off. However, even within the IG space, the ESG benchmark outperformed its non-ESG counterpart. We believe that this is a result of the fact that the J.P. Morgan ESG benchmarks and ESG mandates held greater exposure to higher quality issuers over the stress test period. There appears to be a clear correlation between the ESG score and credit rating, as illustrated in Figure 1 below, which supports the view that incorporating ESG scores could limit downside performance during periods of market stress.

A focus on environmental factors typically also means that an ESG mandate or benchmark would have a lower allocation to commodity producers and oil exporters that screen poorly against ESG metrics. For example, the exclusion of Mexico’s state-owned petroleum company, Petróleos Mexicanos (Pemex), which until mid-April was rated IG by Moody’s but excluded from the ESG benchmarks since it did not meet the minimum criteria, helps explain nearly 20% of the outperformance of the ESG hard currency benchmark. Moreover, the exclusion of some oil exporters from the ESG sovereign HY benchmark, including Nigeria and Angola, helped it to outperform the non-ESG version.

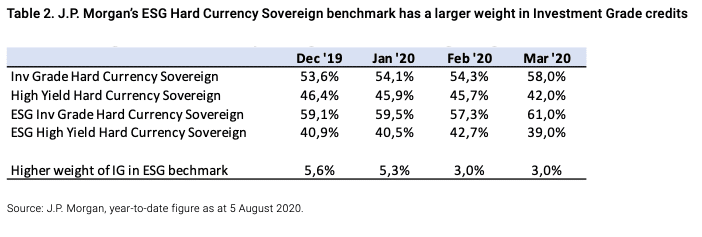

Financial markets experienced an unprecedented recovery in the April through July time frame following the massive policy actions taken by DM and select EM fiscal and monetary authorities in response to the slowdown. However, EM ESG benchmarks, given their higher weighting to IG credits as outlined in Table 2 below, have lagged the broad-based beta rally. Additionally, oil exporting credits that drove the underperformance in March have also been important drivers of the recovery. As an example, the Angolan subcomponent posted a return of over 30% in June as it looked increasingly likely that it would benefit from partial official sector debt forgiveness and after the country decided to tighten its fiscal belts assuming a more realistic budgeted oil price. Overall, the IG component of the ESG indices have had a much better track record than ESG HY, which has had a more difficult time given it still had exposure to distressed sovereign names such as Ecuador, Lebanon, and Argentina which all have idiosyncratic problems. Given that the ESG HY benchmark actually had higher allocations to these countries than the non-ESG version, it illustrates that no benchmark is perfect and that there is still plenty of opportunity for active management.

But active managers did not perform as well as passive managers during this recovery period. While active EM ESG funds in aggregate underperformed their ESG benchmarks in March, hard currency sovereign EM ESG funds, which account for 70% of the USD 2.5 billion in publicly traded daily ESG funds with a J.P. Morgan ESG benchmark we track, actually outperformed their non-ESG benchmark. Looking at average year-to-date performance, all active EM strategies, except the blended ESG mandates, underperformed their ESG benchmarks. We feel that the aggregate underperformance of active managers was likely related to concentrated exposures in countries that became debt restructuring candidates due to the crisis.

We believe that active management of EM fixed income mandates with a strong ESG overlay should be able to differentiate from benchmark returns. During the sharp risk-off period in March 2020, we remained focused on higher quality and higher-rated issuers, employing many of the same bottom-up research principles that we utilize across the firm’s other mandates. We believe that active managers in this space can outperform both passive managers and the ESG benchmark by following two strategies:

- Start with fundamental analysis when evaluating investments for inclusions in an ESG mandate. We believe that you cannot focus on ESG factors alone. Traditional bottom-up analysis, which is required to assess the ability and willingness of an issuer to pay, needs to be applied first. As we saw during the sell-off, enhancing yields of a mandate by moving down the credit spectrum without due regard for credit fundamentals did not prove to be a successful investment strategy. For example, active managers would have benefited from excluding Lebanon and Ecuador from their mandates because of their credit difficulties before March and April, despite these countries still meeting JP Morgan’s score criteria for ESG benchmark inclusion.

- Use of an ESG score as a portfolio screening tool needs to be balanced against real-time world events. Active managers should consider that solely using ESG scores as a screening tool may not perfectly capture cyclical or permanent effects. While some EM issuers may have high ESG scores, they can also make decisions that will negatively impact future scores. And vice versa, low scoring EM issuers can also make critical decisions that will drive improvement to their ESG scores in the future. These decisions typically take time to be reflected in a country’s ESG score. Active managers, who employ a fundamental analysis approach can look to capitalize on this temporary score dislocation, helping to drive performance.

We believe that the recent outperformance of EM ESG benchmarks in March will continue to drive interest in ESG-based investment strategies in EM fixed income going forward. While investors can have greater confidence that EM ESG mandates can perform well during a volatile period, they are right to be concerned whether active management can outperform passive counterparts. To benefit from growing investor inflows into these mandates, we believe that active managers will need to apply fundamental investing principles alongside sustainability to drive performance and differentiate themselves.

This article featured in HedgeNordic’s report “ESG in Alternative Investments.”

Photo by Roman Mager on Unsplash